Call us: 0731-402-8443, 750-900-8989 | Email: infinityservices2018@gmail.com

Definition: Double Entry System refers to the system of bookkeeping that is prevalent at present. According to this system, every transaction has equal and opposite effects, in a minimum number of two accounts.

For Example:

Suppose a firm purchased a laptop for cash Rs. 70,000. The two aspects of this transaction are that the amount of cash is reduced and assets, i.e. laptop comes into the organization.

Hence, in the double-entry system, both aspects of the transaction are entered into the financial books. It is also termed a complete entry system.

As in physics, every action has an equal and opposite reaction. Similarly, in the field of accounting, every transaction results in an equal yet opposite balance in accounts, i.e. debit and credit.

Therefore, the transactions are entered in the financial books as regards debit and credit, wherein debit in a particular account is counterbalanced by the credit in another account. It requires that for different transactions that have occurred during the course of business, the amount entered in the debit, of a particular account must tally with the amount entered in the credit of the corresponding account.

The system was developed by an Italian Mathematician Luca Pacioli, in the year 1494.

Each transaction has two aspects, wherein one receives the benefit while another gives away the benefit. And to keep a systematic record of the transactions, both aspects must be recorded. And the account that receives the benefit is debited whereas the account that foregoes the benefit is credited.

The system is based on the assumption that there won’t be any giving without receiving. Hence, for every debit, there is a corresponding credit. Based on the Double Entry System, the accounting equation can be expressed as:

Owner’s Equity + Outsider’s Equity = Total Assets

Or

Capital + Liabilities = Total Assets

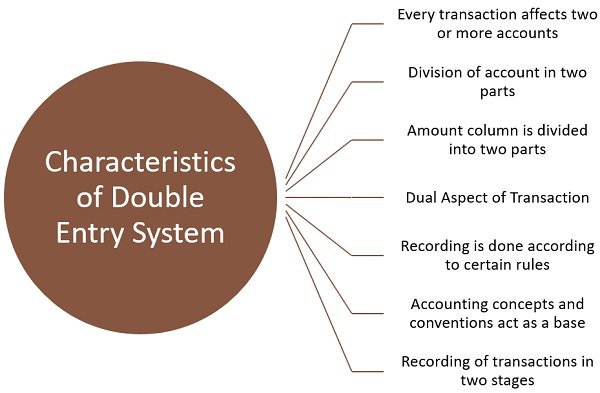

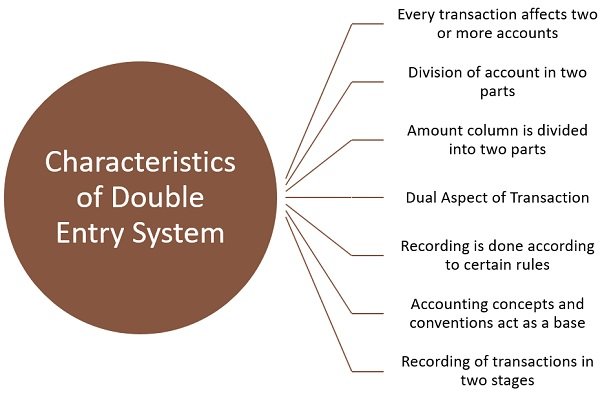

Double Entry System is characterized by:

Every transaction affects two or more accounts: In every business transaction two accounts are involved, wherein one is debited while the other is credited. When one transaction affects multiple accounts, the amount of the accounts which are debited and credited are always equal.

Division of account in two parts: The basis of preparation of ledger accounts are journal and subsidiary books. Each of them has two sides wherein the left side is debit and the right-hand side is credit.

Amount column is divided into two parts: There is a division of the amount column into debit and credit.

Dual Aspect of Transaction: It is based on the notion that every debit has an equivalent credit. That is why they are recorded simultaneously on the debit and credit sides.

Recording is done according to certain rules: There are golden rules of accounting on the basis of which the recording of transactions is made in the books of accounts. These are basically rules for debit and credit.

Accounting concepts and conventions act as a base: Double Entry System of bookkeeping relies on the universally accepted conventions and concepts, which are required to be followed while maintaining accounting books.

Recording of transactions in two stages: It enables the recording of transactions at two stages – initially in a detailed manner and then in a summarized manner, which brings correctness of recording and generating accounting information.

206, Prem Plaza, opp. Canara Bank, Bhawar kuan, Indore - 452001 (M.P.)

+91 7509008989 +91 8007951977 infinityservices2018@gmail.comMon – Sat 9:00A.M. – 8:00P.M.

Contact Us

{kind=link}